The Importance of Due Diligence

When investing in real estate proper due diligence is one of the most important keys to success. There are many issues that can arrive after closing that could have been prevented with a little homework. Thankfully, many professional underwriters and lending companies will aide in this endeavor once a contract has been accepted.

The due diligence period generally refers to a set amount of time one has to investigate the aspects of the property after a contract is accepted and before closing. During this time the buyer may back out of the contract for any reason without repercussions. Generally, the length of time is pre-determined by either the state (usually 10-15+ days) or agreed upon in the contract and begins when escrow is opened.

Every lender and title company will have a set list of what they require to complete what they believe is proper due diligence on an investment. This not only protects them but you as the buyer. However, not everyone’s requirements and parameters are the same. A private individual lender may require very little due diligence to be done while the bank will have you jumping through hoops. Knowing what to look for and expect is crucial in this business regardless of if you are doing it all yourself or leveraging your team.

Buyer’s Due Diligence

- Physical Inspection – plumbing, structural, roof, HVAC, pests, septic, well, etc.

- Crime (including sex offender) statistics

- Upcoming building plans in the neighboring area / Zoning

- Talk with neighbors to get the inside scoop on the area

- Median Household Income

- Surrounding Rental Rates

- School Rankings

- Repair Quotes (if applicable)

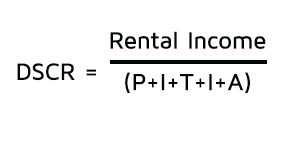

- Estimate your Debt to Service Coverage Ratio – DSCR (if applicable)

- Review of Seller’s Disclosures

- Property Rights

- Submit all requested documents to lender

- Review all legal documents for accuracy and understanding

Lender’s Due Diligence

- Review of all documents for accuracy and suitability

- Contract / Assignment – review terms and make sure the seller has the right to sell property etc.

- Deed or Proof of Ownership – review chain of custody

- Interior and Exterior Photos

- Scope of Work / Lease Agreements

- Bank Statements

- Background Checks – this can include criminal, credit, tax liens, death index, bankruptcy, lawsuit history, etc.

- Insurance Quotes – verify amount, terms, address, type (hazard, flood, windstorm, vacant, occupied, builder’s risk, commercial etc), and insured names

- Flood Determination – what flood zone does the property lie in

- Corporate Docs (if applicable)

- Certificate of Formation

- Certificate of Filing

- Operating Agreements

- Amendments

- Resolutions

- FEIN or W-9

- Entity Search – verify the entity is active and managing members

- Driver’s License (state ID’s) – citizenship

- Social Security or W-9

- Contact Information from borrower

- Appraisal / Survey – Value of property and boundary lines

- Permits

- Homeowners Association (HOA) – restrictions and verify dues are up to date

- Verify Taxes are Current and that there are no liens

- Review of Title Commitment

- Legal Descriptions

- Policy Amount

- Encroachments / Easements

- Liens – Verify Clear Title / Judgements

- Review of Loan Package and Closing Disclosure

Commercial

- Phase 1 Environmental (if applicable) and Phase 2 if needed

- Proposed Plat Changes

- Drawings / Spec’s

- Executive Summary

- Rent Roll

- Feasibility Study

- Pro-Forma P&L

Ready to Invest?

This list is in no way meant to be used as a complete guide to due diligence, but it aims to serve as a starting point. There are many things to consider when investing in real estate and are often driven by one’s school of thought. Asset based lenders vs. credit-based lenders will have varying requirements, as well those investors who invest in fix-n-flip, rental, and commercial loans. The bottom line here is to do your homework throughout the entire process. Make sure you ask lots of questions and that you understand the legal documentation you are signing. Consult with your lawyer or financial advisor if you have questions or are still unsure. Don’t be afraid to walk away from a deal if you find an issue during the due diligence period that the seller refuses to fix or can’t. Better to lose a small sum of cash than to get in over your head. Be sure to partner up with a lender that you can trust. Now that you are armed with this knowledge, get out there and find some deals!

Investor Loan Source, a hard money lending company, provides high-quality investment property loans to private real estate investors at the lowest costs possible. Our process for providing real estate investors with private lending is unique. We place emphasis on the hard asset and value of the collateral (property) and less on the borrower. Our asset-based real estate investment loan model means we can provide more money lending to more investors than is available from standard bank loan models. At Investor Loan Source, providing real estate investors hard money loans is our business; it’s all we do. We offer several business real estate loans products designed to serve a variety of investors and property profiles, including hard money lending for properties to sell on owner finance.

To learn more about Investor Loan Source, visit our website or follow us on LinkedIn, Facebook, and Twitter. To apply for a loan, click HERE.