When it comes to real estate investing, a thorough understanding of the capital stack is essential for success. The capital stack is the collective term for the various sources of capital used to finance a commercial real estate project. Understanding the different parts of the capital stack and how they work together can help you make informed decisions when investing in commercial real estate. In this blog post, we’ll discuss the components of the capital stack and how they come together to fund a development or redevelopment project.

What is a Capital Stack?

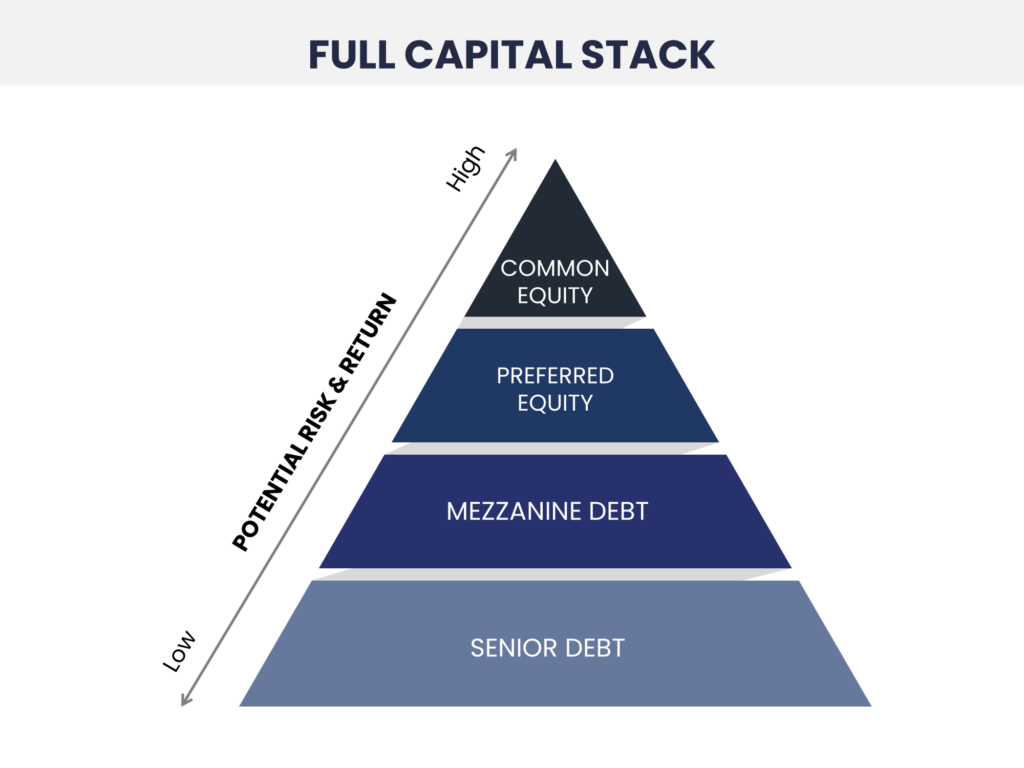

The “capital stack” refers to the different types of financing used to fund a given CRE (Commercial Real Estate) investment. It is the combined set of all financing instruments that investors use to acquire and develop CRE investments with mention to their risk and return profile. The capital stack for any real estate transaction typically involves numerous parties and a variety of structures, offering investors creativity and freedom in how they structure the deal. The instruments used in the capital stack are commonly referred to as common equity, preferred equity, mezzanine debt, and senior debt. Understanding the potential and risks for each layer can help investors understand how to build wealth by adequately funding their commercial real estate deals.

Senior Debt

Senior debt is a critical component of the capital stack in commercial real estate investing, with secured debt providing lenders a sense of security and investors an opportunity to build wealth. Senior debt is secured by a mortgage or deed of trust on the property itself, making it the base of the capital stack. If the borrower fails to pay, the senior debt holder can take over the property and recoup their investment by selling the property or selling the non-performing loan. However, this lower level of risk comes with a lower yield than all other positions on the capital stack.

Mezzanine Debt

Mezzanine debt comprises the next layer of the capital stack and follows the senior debt in payment priority. After the developer has paid operating expenses and senior debt, the borrower must pay the mezzanine debt. Because mezzanine debt sits above the old debt in priority of payment, this higher risk to lenders leads to higher returns, as borrowers typically pay higher interest rates for mezzanine loans.

For mezzanine loans, if a borrower fails to pay and defaults, the lender can also take possession of the property, typically agreeing with the senior debt holder on how each entity’s rights will be protected.

Preferred Equity

Because of the creative potential of preferred equity investments in the capital stack, it is impossible to define one shape it may take. Preferred equity is very flexible, allowing investors to take different positions. For example, a “hard” preferred equity position functions similarly to a mezzanine loan with a fixed maturity date and payment schedule. A “soft” position will likely include returns based on the project’s performance. Understandably, hard preferred returns range similarly to mezzanine loans and share similar rights in case of default. In contrast, soft preferred equity holders have fewer rights but the potential for higher returns –especially for projects that perform better than anticipated because this equity is “preferred.” It is paid before any common equity distributions can be made.

Common Equity

At the top of the stack and the riskiest position, common equity is the most profitable position on the stack. Typically, the lender or other equity investors require the borrower to invest some portion of their own capital in the project, thereby having skin in the game and a vested interest in seeing the project succeed. In addition, common equity positions also require that every other capital investment be repaid before common equity sees returns. However, if the property performs well, common equity investors often have no limit to potential returns. Common equity returns can also be creatively divided between investors, but often the developer or sponsor of the project sees considerable common equity returns.

Investor Loan Source, a private money lending company, provides high-quality investment property loans to private real estate investors at the lowest costs possible. Our process for providing real estate investors with private lending is unique. We place emphasis on the hard asset and value of the collateral (property) and less on the borrower. Our asset-based real estate investment loan model means we can provide more money lending to more investors than is available from standard bank loan models. At Investor Loan Source, providing real estate investors hard money loans is our business; it’s all we do. We offer several business real estate loan products designed to serve a variety of investors and property profiles, including private money lending for properties to sell on owner finance.

To learn more about Investor Loan Source, visit our website or follow us on LinkedIn, Facebook, and Twitter. To apply for a loan, click HERE.Categories